The trouble with Ostarine: Jimmy Wallhead’s

16th March 2018

Features

Allegations have resurfaced which suggest that Rangers should not have been awarded a UEFA licence for the 2011/12 season due to overdue payables to Her Majesty’s Revenue & Customs (HMRC), prohibited by UEFA regulations. The Scottish Football Association (SFA), however, insists that the licence was correctly issued. The allegations centre around two offshore tax schemes set up by Rangers, one of which is still subject to court proceedings, and the date when a ‘potential’ HMRC tax liability became ‘actual’.

Historically, two Glasgow-based clubs – Celtic and Rangers – have dominated Scottish football. Rangers Football Club PLC (Rangers PLC) was placed into administration in February 2012 and liquidated at the end of the 2011/12 season. The assets of the club were then sold to new owners (Sevco Scotland Ltd.). In June 2012, and the club was renamed The Rangers Football Club Ltd. (Rangers Limited), however the Scottish Premier League (SPL) voted against accepting Rangers into its league. The Scottish Football League (SFL) voted to accept Rangers into its Third Division in the 2012/13 season rather than its First Division, as the SFA and SPL had sought. In 2013, the SPL and SFL merged to become the Scottish Professional Football League (SPFL).

In March this year, a complaint (PDF below) was filed with UEFA alleging collusion between the SFA and Rangers in order to ‘ensure that one club gains financially at the expense of others’. In essence, the complaint alleges that the SFA and Rangers colluded to allow Rangers to be awarded a licence to compete in the lucrative Champions League during the 2011/12 season, despite knowledge that due to overdue payables to HMRC, the licence should not have been granted.

It has been further alleged that SFA decisions allowed a commission of inquiry into the financial collapse of Rangers to be misled; that the SFA failed to investigate whether the UEFA licence was correctly granted; and that journalists were misled in order to cover up irregularities in granting the licence. UEFA, however, insists that the licence was correctly issued.

‘On 19 April 2011, the SFA granted the licence necessary for participation in the 2011/12 UEFA club competitions to Rangers FC and this decision was communicated to the UEFA administration on 26 May 2011’, read a 8 June 2016 UEFA letter (PDF below). ‘At the time when the licence was granted by the SFA, there was no reason for UEFA to suspect any irregularity committed either by Rangers FC or by the licensor (SFA). Moreover, and simply or the sake of completeness, we can also advise that there is a five-year limitation period to investigate any possible breach of the club licensing regulations and so UEFA is not, in any event, in a position to open any investigation with regard to a licence granted in April 2011, since this would be time-barred’.

UEFA was initially notified of the complaint in February, however was sent detail regarding the specific allegations in March. A brief summary is as follows:

• That as Her Majesty’s Revenue & Customs (HMRC) considered Rangers PLC to have an overdue tax liability in February 2011, SFA officials knew about and withheld knowledge of overdue payables at Rangers which would have resulted in the club being ineligible for a UEFA licence for the 2011/12 season;

• That Rangers PLC accepted its £2.8 million liability to HMRC on 21 March 2011, ahead of the 31 March 2011 deadline stipulated by the UEFA Club Licensing and Financial Fair Play (CLFFP) Regulations.

• That the SFA ignored its own rules by allowing Dave King and Paul Murray to become Directors of Rangers Limited in 2015, despite both having been on the board of Directors at the Rangers PLC in 2012, when the club entered liquidation. Article 10.2(j) of the SFA’s Articles of Association prevented anyone from becoming a Director at a Scottish club if, during the previous five years, they had been a Director at a club that entered insolvency;

• That the SFA broke its own rules by allowing Dave King to become a Director of the Rangers Limited in March 2015, despite his pleading guilty in 2013 to 41 of 322 charges of tax fraud brought by the South African Revenue Service (SARS);

• That the date of the LNS inquiry, which was initially supposed to start in 1998, was changed to 2000-2011. This had the effect of excluding the first of two offshore schemes allegedly set up by Rangers PLC to pay players and staff whilst avoiding tax – a scheme in which the President of the SFA at the time, Campbell Ogilvie, was involved with whilst working as Company Secretary at the club;

• That the SFA allowed Campbell Ogilvie to continue as SFA President during the ‘independent’ LNS inquiry, despite the fact that he had served as a Director of Rangers PLC during the period being investigated.

Since 2011, UEFA Club Licensing and Financial Fair Play (CLFFP) Regulations have required clubs to prove that they have no overdue payables in order to be awarded a licence to compete in European competitions. ‘Financial fair play was approved in 2010 and the first assessments kicked off in 2011’ reads a UEFA Q&A section on the regulations. ‘Since then, clubs that have qualified for UEFA competitions have to prove they do not have overdue payables towards other clubs, their players and social/tax authorities throughout the season. In other words, they have to prove they have paid their bills.’

This provision is outlined in Articles 49 and 50 of the 2010 edition of the Club Licensing and Financial Fair Play Regulations, which would have been in force at the time that Rangers PLC sought a licence to compete in European competition. They state that clubs must demonstrate no overdue payables ‘as at 31 March preceding the licence season’ – the UEFA club competitions begin at the end of June.

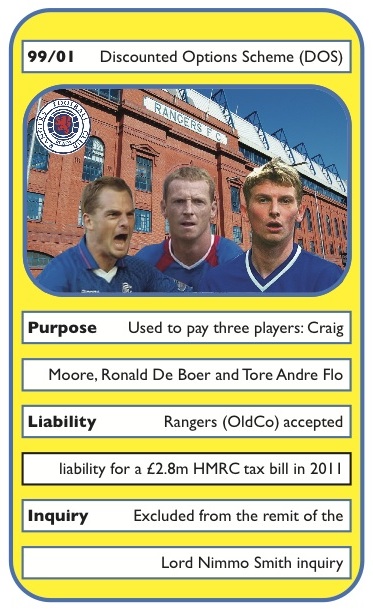

Annexed evidence (PDF below) published by The Offshore Game (TOG), an offshoot of the Tax Justice Network (TJN), reveals that Rangers PLC had been in discussion with HMRC about its Discounted Options Scheme (DOS) since 2000. The DOS scheme created offshore shell companies which were invested in by the Rangers Employee Benefits Trust (REBT), which was created in 1999. In return, the REBT would have the option to take control of the shell companies in the future. This made them technically worthless to anyone other than the REBT, however REBT would allow its option to take control of the companies to expire, passing ownership of the company – and the money invested in it – to Rangers players.

As the Panama Papers leaks revealed, Rangers PLC was not unique in using such a system.  Such schemes appear to have been commonly used by clubs to pay players. The Panama Papers show that Real Sociedad set up offshore companies for seven players between 2000 and 2008; that

Such schemes appear to have been commonly used by clubs to pay players. The Panama Papers show that Real Sociedad set up offshore companies for seven players between 2000 and 2008; that  20 football club owners set up offshore companies through law firm Mossack Fonseca; and almost 20 footballers set up similar companies.

20 football club owners set up offshore companies through law firm Mossack Fonseca; and almost 20 footballers set up similar companies.

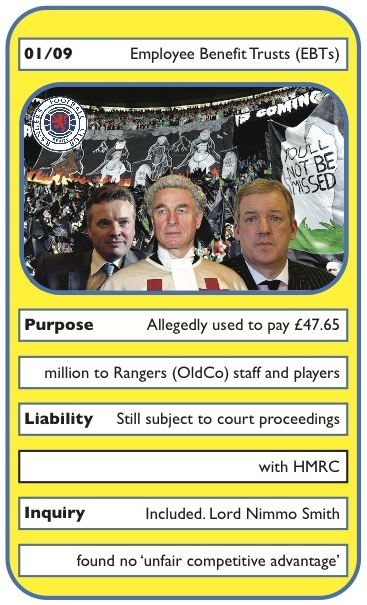

Evidence from TOG (PDF below) states that the Rangers DOS scheme only set up shell companies for three players – Craig Moore, Ronald De Boer and Tore Andre Flo. A more complex scheme was later set up and used from the 2001/2 to 2008/9 tax years. In November 2015, the Scottish Court of Session upheld an appeal by HMRC arguing that the later scheme was ‘designed to avoid the payment of income tax and National Insurance Contributions (NICs)’. As this later scheme is still subject to court proceedings, it doesn’t yet constitute an ‘overdue payable’ under UEFA’s CLFFP Regulations – but only because it has yet to be decided whether an ‘overdue payable’ is actually due.

As previously mentioned, evidence in a report compiled by The Offshore Game (TOG) appears to indicate Rangers’ acceptance of the overdue liability to HMRC prior to the 31 March 2011 deadline specified in the UEFA CLFFP Regulations. TOG have agreed that we can reproduce the report, which is included in PDF format below. It has been argued that this acceptance qualifies the DOS scheme as an ‘overdue payable’ within the meaning of the UEFA CLFFP Regulations.

The timing of this acceptance is crucial. As previously explained, the CLFFP Regulations require clubs to report any overdue payables ‘as at 31 March preceding the licence season’. Rangers PLC reported that it had a ‘potential’ tax liability to the SFA despite having apparently accepted liability for the £2.8 million owed to HMRC on 21 March 2011. It was required to declare overdue payables as of 31 March 2011 under the CLFFP Regulations and TOG, following their evidence, argue that the liability was actual, not ‘potential’, as Rangers PLC claimed.

A licence was issued to Rangers PLC on the basis that the ‘potential’ liability was not an overdue payment under the terms of the UEFA rules. It has been alleged by TOG and the UEFA complaint that this licence was granted despite the SFA knowing that Rangers PLC had accepted its liability to HMRC. SFA President Campbell Ogilvie had been an employee of the club from 1978 to 2005 and was a Rangers PLC Director when the DOS and its successor were set up. He became the SFA’s first Vice President in 2007 and was later promoted to SFA President in June 2011.

Annex VI of TOG’s report contained a 5 May 2011 letter sent by HMRC to Murray International Holdings, then owner of Rangers PLC, about the payment of the £2.8 million. ‘I agreed with Mr. McIntyre that as I saw no grounds for appeal, as the liability is agreed, I would await developments regarding a potential takeover but as considerable time has passed I cannot allow this to drift any more’, wrote HMRC in the letter, also contained within TOG’s evidence, and reproduced below.

Donald McIntyre was Company Secretary at Rangers PLC at the time. On 21 March 2011, Murray International Holdings’ (MIH) Finance Director, Mike McGill, held a meeting with HMRC at which he presented Rangers PLC’s proposal that they would pay the owned £2.8 million to HMRC. On a spreadsheet detailing the agreed payment to HMRC, a handwritten note from ‘DM’ advises that HMRC have accepted Rangers PLC’s offer of payment ‘in principle’.

The letter signed off by McIntyre and McGill was in response to a suggestion to settle with HMRC by Rangers PLC’s tax Barrister, Andrew Thornhill, in a 3 March 2011 letter, also in Annex VI to TOG’s report, reproduced below. ‘The scheme was carried out in such a way which suggests that arguing the case would be an uphill task’, Thornhill advises. ‘However, the deciding factor in favour of settling the matter is the existence of side letters in two instances demonstrating that there was a true intention of putting case into the hands of the players as part of the remuneration package. It does not help either the existence of these letters has been denied or not revealed by the club. In this state of affairs, it would be sensible to seek a settlement.’

The SFA said that the UEFA complaint had been launched by Celtic supporters who do not want Rangers back in the Scottish Premier League, which Rangers Limited is competing in after winning the 2015/16 Scottish Championship. It is true that Celtic supporters have complained about the situation.

This summer, SFA CEO Stewart Regan told the Daily Record that the SFA had nothing to fear from ‘Resolution 12’, passed at a November 2013 Celtic AGM (PDF below), which requested that UEFA ‘undertake a review and investigate the SFA’s implementation of UEFA & SFA license compliance requirements, with regard to qualification, administration and granting of licenses to compete in football competitions under both SFA and UEFA jurisdiction, since the implementation of the Club Licensing and Financial Fair Play Regulations of 2010’.

“The UEFA licence was granted appropriately”, said an SFA spokesperson. “The awarding of the licence was accepted by the Celtic AGM”. That has not stopped Celtic fans seeking to place newspaper adverts urging UEFA to intervene. “The basis on which the UEFA licence was granted to Rangers was correct; it was based on the evidence provided and the evidence submitted by the club, by HMRC and by lawyers acting on behalf of the club and it outlines the timeline of the liability”, continued the spokesperson.

The SFA spokesperson claimed that it was not involved in the decision to grant Rangers the UEFA licence, as that was a decision for Scotland’s clubs to make. However, under UEFA regulations, each member association ‘remains liable and responsible for the proper implementation of the club licensing system, regardless of whether there is delegation or not’.

The SFA pointed The Sports Integrity Initiative to an article written by David Conn for The Guardian, which quoted an ‘informed source’ as confirming that HMRC had agreed that the overdue £2.8 million did not need to be paid until after the 31 March deadline for overdue payables – i.e. after Craig Whyte’s May 2011 takeover of the club. Annex IX UEFA’s CLFFP Regulations do allow a club to write off an overdue payable if a club can prove by 31 March that it:

• has concluded an agreement which has been accepted in writing by the creditor to extend the deadline for payment beyond the applicable deadline (note: the fact that a creditor may not have requested payment of an amount does not constitute an extension of the deadline); or

• it has brought a legal claim which has been deemed admissible by the competent authority under national law or has opened proceedings with the national or international football authorities or relevant arbitration tribunal contesting liability in relation to the overdue payables.

If Rangers PLC had not agreed the final bill with HMRC on 31 March 2011, there would not be a case to answer. However as shown above, signed documents within TOG’s report suggest that Rangers PLC accepted liability for the overdue Bill on 21 March 2011.

A 2 April 2011 article from the Daily Record claimed that the HMRC bill ‘dropped through the Ibrox front door only three weeks ago’, which suggests that Rangers PLC may have known about its liability to HMRC ahead of the 31 March deadline. However, Rangers PLC appears to have failed to add an addendum to its interim accounts to reflect that what was a ‘potential’ liability as at 31 December 2010 had since become an actual liability to HMRC.

‘The exceptional item reflects a provision for a potential tax liability in relation to a Discounted Option Scheme associated with player contributions between 1999 and 2003’, read Rangers’ interim results. ‘Discussions are continuing with HMRC to establish a resolution to the assessments raised’. This was true at 31 December 2010, but according to the documents within TOG’s report, it appears that these discussions had been completed prior to the 1 April 2011 filing of these accounts.

As the interim accounts were for the year end 2010, the liability at that point in time was potential, however it is understood that it is common practice that if there is a significant event between the year end and the accounts being signed off (i.e. the ‘potential’ liability becoming ‘actual’), then that is normally noted as a post-balance sheet event in a separate part of the accounts. As the accounts were unaudited interim accounts, it is therefore unclear if any rules have been broken by this failure to mention Rangers PLC’s alleged acceptance of the HMRC liability on 21 March 2011.

Article 66 of the UEFA CLFFP Regulations places a secondary requirement on a club to prove that it had no overdue payables ‘as at 30 June of the year in which the UEFA club competitions commence’. TOG’s evidence and Emails indicate that by 30 June, Rangers PLC had accepted liability for the £2.8 million overdue payable, however described it as ‘postponed’, despite the fact that it had accepted that liability on 21 March 2011 and it only remained for a schedule for payment to be agreed with HMRC.

The SFA has told The Sports Integrity Initiative that confidential HMRC documents relating to the second scheme used from the 2001/2 to 2008/9 tax years prove that HMRC had agreed for the £2.8 million HMRC liability to be postponed until after Craig Whyte’s takeover of the club in May 2011.

An SFA response to The Sports Integrity Initiative, sent via email, was copied from a letter sent by Celtic shareholders to the SFA on 20 April 2016, in which they accepted that the 2011/12 licence was correctly awarded. ‘The information contained in our initial letter was not referred to you for the purposes of reviewing the initial grant of the UEFA Licence, which our clients have always believed to be valid’, it read (PDF below). ‘Accordingly, your letter of 14th March appears to miss the point and fails to address the issues which were raised and which concern the licensing process and activity post 31st March and a potential breach of the CFCB regulations in relation to compliance with regulation 66 and other provisions’.

‘In respect of overdue payments for the season in question, licence applicants had to prove that as at 31 March 2011 they had no overdue payables relating to transfer activities occurring prior to 31 December 2010 or towards employees or social and tax authorities as a result of contractual and legal obligations towards their employees that arose prior to 31 December 2010’, wrote UEFA in its 8 June letter. As TOG’s report suggests that Rangers PLC had accepted liability for the £2.8 million HMRC bill on 21 March 2011, which related to the DOS scheme in operation from 1999/2000 until 2000/2001, it would appear that the club did have an obligation to declare an overdue payable at 31 March 2011.

UEFA argues in its 8 June letter that it is ‘time-barred’ from investigating the issue of the awarding of the 2011/12 UEFA licence to Rangers PLC. Article 67 of the 2010 CLFFP Regulations in force at the time reads: ‘The licensee must promptly notify the licensor in writing about any significant changes including, but not limited to, subsequent events of major economic importance until at least the end of the licence season. The information prepared by management must include a description of the nature of the event or condition and an estimate of its financial effect, or a statement (with supporting reasons) that such an estimate cannot be made.’ Article 71 of the same regulations allows UEFA to ‘at any time, conduct compliance audits of the licensor and, in the presence of the latter, of the licence applicant/licensee. Compliance audits aim to ensure that the licensor, as well as the licence applicant/licensee, have fulfilled their obligations and that the licence was correctly awarded at the time of the final decision of the licensor.’

However, Article 10 UEFA’s Disciplinary Regulations does contain such a statue of limitations. It reads: ‘There is a statute of limitations on prosecution, which is time-barred after:

a. one year for offences committed on the field of play or in its immediate vicinity;

b. ten years for doping offences;

c. five years for all other offences.

Match-fixing, bribery and corruption are not subject to a statute of limitations.’

So it would appear that UEFA’s Regulations block any further investigation of the issue of the 2011/12 club licence to Rangers PLC. UEFA’s 8 June letter also said that ‘if Rangers FC had been in breach of the enhanced overdue payables rule as of 30 June or 30 September 2011, any eventual sanctions would have related to potential participation in the 2012/13 UEFA club competitions, with no impact on the club’s participation in the 2011/12 UEFA Champions League’. As such, UEFA concludes ‘there is clearly no need for UEFA to investigate this matter any further since the club was not granted a licence to participate in the 2012/13 UEFA club competitions, the new club/company entered the fourth tier of Scottish football and it was not able to play in UEFA competitions for the next three years in any event’.

A number of questions remain, however:

• Did Rangers PLC tell the SFA about the nature of the £2.8 million liability to HMRC?

• What did Rangers tell the SFA?

• Why would HMRC postpone the £2.8 million liability until after Whyte’s takeover of the club if, as the SFA asserts, it was ‘potential’?

Though UEFA may no longer have the capacity to investigate, these nonetheless remain important questions for the sake of transparency.

On 5 March 2012, the Scottish Premier League announced that ‘The SPL Board has instructed an investigation into the alleged non-disclosure to the SPL of payments made by or on behalf of Rangers FC to players since July 1, 1998’. The SFA had earlier announced that it had appointed Lord Nimmo Smith to head the four-man panel conducting the Independent Inquiry, as well as SFA CEO Stewart Regan. As can be seen from the PDF of the Inquiry’s conclusions below, at some point its scope was changed to only consider payments made to players after 2000.

The alleged effect of this was to exclude the DOS scheme – which Rangers PLC had accepted liability for – from the scope of the Inquiry. As previously explained, the later scheme, which ran from 2001/2, is still subject to court proceedings, and therefore cannot yet be considered an ‘overdue payable’ within the remit of the CLFFP Regulations. In more basic terms, until court proceedings are concluded, it has yet to be decided if an ‘overdue payable’ is due. Therefore even if Rangers PLC is in the clear regarding the DOS scheme, it could still face potential sanctions over the latter scheme.

Lord Nimmo Smith concluded that between 2000 and 2011, Rangers PLC (OldCo) ‘entered into side-letter arrangements with a large number of its professional players under which Oldco undertook to make very substantial payments to an offshore employee benefit remuneration trust, with the intent that such payments should be used to fund payments to be made to such players in the form of loans’. He also found that such agreements ‘were required to be disclosed under the SPL and SFA rules as forming part of the players’ financial entitlement and as agreements providing for payments to be received by the players’ and that ‘OldCo through its senior management decided that such side-letter arrangements should not be disclosed to the football authorities’.

Crucially, Nimmo Smith found that ‘Rangers FC did not gain any unfair competitive advantage from the contraventions of the SPL Rules in failing to make proper disclosure of the side-letter arrangements, nor did the non-disclosure have the effect that any of the registered players were ineligible to play, and for this and other reasons no sporting sanction or penalty should be imposed upon Rangers FC’. However, it could be argued that if it had considered the earlier DOS scheme, its conclusions might have been different, since Rangers PLC had apparently accepted liability for an ‘overdue payable’ to HMRC in respect of the DOS scheme, which brings that ‘overdue payable’ within the remit of UEFA’s CLFFP Regulations. Champions League football and the financial solidarity payments it brings from UEFA arguably might be seen as a ‘sporting advantage’ gained from failure to disclose such a scheme to the SFA and SPL.

‘Each domestic champion which did not qualify for the group stage received €200,000’, reads a UEFA statement concerning the season in question. The SFA also received €690,000 from Rangers’ participation in the 2011/12 Champions League.

Both the UEFA complaint and the evidence compiled by TOG allege that the SFA failed to fully investigate Rangers PLC’s ‘potential’ tax liability. As the remit of the Nimmo Smith inquiry meant that it was required to only consider the later scheme, SFA President Campbell Ogilvie was able to confirm – entirely accurately – that: “I assumed that all contributions to the Trust were being made legally, and that any relevant football regulations were being complied with. I do not recall contributions to the Trust being discussed in any detail, if at all, at Board meetings. In any event, Board meetings had become less and less frequent by my later years at Rangers. Nothing to do with the contributions being made to the Trust fell within the scope of my remit at Rangers.”

However, the allegation is that he should have mentioned the earlier DOS scheme that Rangers PLC had accepted liability for in March 2011. Contained in Annex III of TOG’s evidence is a 3 September 1999 letter signed by Ogilvie on behalf of the club, under which OldCo took control of Montreal Limited, an Isle of Man company managed by Allied Irish Bank. In the letter, Ogilvie makes it clear that the purpose of the company is to provide remuneration to a Rangers PLC employee.

To be clear, there is no suggestion that SFA President Ogilvie has done anything illegal. However, it has been suggested by TOG that the fact that he did not mention the earlier DOS scheme to the Nimmo Smith Inquiry gives the appearance that the SFA may have ‘managed’ the Inquiry. The SFA appointed its CEO, Stewart Regan, to the ‘independent’ LNS inquiry despite Ogilvie, his superior at the SFA, having served as a Director of Rangers PLC during the period being investigated. Given the sensitivity of the issue under inquiry, Mr Regan’s appointment may appear a little surprising to impartial observers.

When questioned by The Sports Integrity Initiative, the SFA said that the UEFA complaint and TOG had “conflated” the DOS scheme with the later scheme considered by the Lord Nimmo Smith Inquiry. The SFA are correct in that Nimmo Smith was asked to examine the later scheme, but the change in the dates of the initial inquiry from 1998 to 2000 precluded him from examining the DOS scheme (which Campbell Ogilvie was allegedly involved with).

To recap, the allegation is that the SFA ignored its own rules by allowing Dave King and Paul Murray to become Directors of Rangers Limited in March 2015, despite both having been on the board of Directors at Rangers PLC in 2012, when the club entered liquidation. A separate allegation is that the SFA broke its own rules by allowing King to become a Director, as in 2013 he had pleaded guilty to 41 or 322 charges of tax fraud brought against him by the South African Revenue Service (SARS).

The SFA defended its decision. “It is not our place to confirm South African law, but he made a positive settlement with them, so on that basis, that could not have been an obstacle to him being considered fit and proper”, said an SFA spokesperson. “Had we said no, we would have become subject to judicial review and we would have lost”. The SFA also denied that Campbell Ogilvie had sat on the panel that made the decision regarding King, despite newspaper articles suggesting otherwise.

There is nothing new in these allegations. It is important to stress that the SFA asserts it has done nothing wrong and UEFA’s position is that Rangers PLC’s licence for the 2011/12 season was correctly issued. However, as the complaint to UEFA in March this year, TOG’s evidence and the continued persistence from backers of Celtic’s Resolution 12 illustrate, many still feel that the issue of this licence is an issue that requires further investigation.

That the SFA appointed its own CEO (Regan) to the independent Lord Nimmo Smith Inquiry into the liquidation of Rangers also appears curious, as his superior was Campbell Ogilvie, who had been involved in the setting up of the DOS scheme that had led to Rangers’ admitted liability to HMRC. There is also the question as to why the dates of the LNS inquiry were moved from 1998 to 2000, excluding the DOS scheme.

Why were Directors of the Rangers PLC allowed to assume new positions at Rangers Limited, despite SFA rules preventing people from becoming a Director at a Scottish club if, during the previous five years, they had been a Director at a club that entered insolvency? It is also difficult to understand how and why Dave King was cleared as a ‘fit and proper person’ given the South African tax offences to which he apparently pleaded guilty.

Why was Campbell Ogilvie, a former Rangers employee, allowed to sit on the Panel that made the decision in King’s case? The SFA’s 11-man Professional Game Board was allegedly excluded from the King decision – if that is true, why were they excluded?

Rangers and Celtic are by far the most popular clubs in Scotland and generate masses of revenue for the SFA and the SPFL. According to Deloitte, Celtic made up 50% of SPL revenue in 2014/15. It is not difficult to understand why some may argue that a motive existed to get Rangers back to the SPL as soon as possible to increase revenue. Indeed, there is some evidence to suggest that pressure was put on SFL clubs to vote to accept Rangers into the First Division back in 2012.

Rangers PLC entered the 2011/12 UEFA Champions League after winning the SPL on goal difference, which the March complaint to UEFA argued deprived another Scottish club of potential revenue and allowed a weakened Rangers side to compete in European competition. Celtic would have been Rangers’ replacement, so Resolution 12 of its AGM, which asked UEFA to investigate this situation – appears to have been based on legitimate concerns.

The people behind the UEFA complaint stress that they are not Celtic supporters. Whether or not that is true, they understandably want to remain anonymous because of the potential threat to them for highlighting these issues.

In 2014, Parma was denied a UEFA club licence by the Italian football association (FIGC) over an unpaid €300,000 tax bill. At the end of 2012, UEFA sanctioned a number of clubs with exclusion from European competition due to ‘overdue payables’ remaining. Earlier this year, it excluded Galatasaray after it failed to comply with the terms of an earlier settlement agreement with UEFA.

Statutes of limitations within UEFA’s regulations may prevent it from investigating whether the 2011/12 licence was correctly issued to Rangers, however the allegations outlined above appear to have a scope that is wider than UEFA club licensing. At the very least, the allegations and evidence outlined within this article suggest that the inquiry into the financial collapse of Rangers PLC may not have been as independent as it could have been. The March complaint filed with UEFA and Celtic shareholders argue that the way in which the situation was handled undermines the integrity of Scottish football governance. That is why The Sports Integrity Initiative decided to investigate this issue.

UEFA has had a busy time recently. It remains to be seen whether it will revisit such allegations, which sit within a complex and inflammatory regulatory environment. However, just because they sit within the historical rivalry between Celtic and Rangers doesn’t automatically mean that the allegations are without merit. Unless a full independent investigation is carried out, these allegations – whether they ultimately have any substance to them or not – appear likely to continue to cast a shadow over Scottish football.

Athletes have been medically harmed due to sport’s limits on testosterone in its female category,...

• Twenty three athletes from 14 countries, competing in 11 sports, were involved in anti-doping...

• Twelve athletes from nine countries, competing in seven sports, were involved in anti-doping proceedings...